One easy way to draw attention to an opinion piece is with a “hot take” or two that change some widely-held belief. This is an especially popular gambit if that belief is held by the left.

Financial journalist Roger Lowenstein did that recently in the Washington Post, when he challenged the widely-held opinion that Lloyd Blankfein, outgoing CEO of Goldman Sachs, is a bad person who has done a great deal of harm to the economy. In this case, the wisdom of crowds got it right.

Lowenstein should know better. His recent commentary on Elon Musk, whom he described as a “a one-person corporate inequality machine,” was pointed and smart. His piece on the “myth of the superhero executive” was an excellent summary of our broken system of executive compensation.

Unfortunately, Lowenstein’s hagiographic treatment of Blankfein hearkens back to his regrettable 2010 profile of another Wall Street miscreant, the hypersensitive JPMorgan Chase CEO Jamie Dimon. And his unwillingness to even mention the rampant fraud at Goldman Sachs under Blankfein’s leadership recalls his unsuccessful 2011 attempt to absolve Wall Street of its criminality.

A response is warranted.

Hot takes

Yes, Lowenstein concedes, Blankfein was paid “tens of millions every year” while his firm “catered to the wealthiest of Americans.” But – wait for the hot take – Lowenstein then says that “the country could use more people like Blankfein.”

Why? Because, writes Lowenstein, “economic inequality is not the best yardstick” for measuring the health of the economy. Instead, he says, “we should be paying attention to… social mobility.”

That’s Hot Take Number Two, apparently.

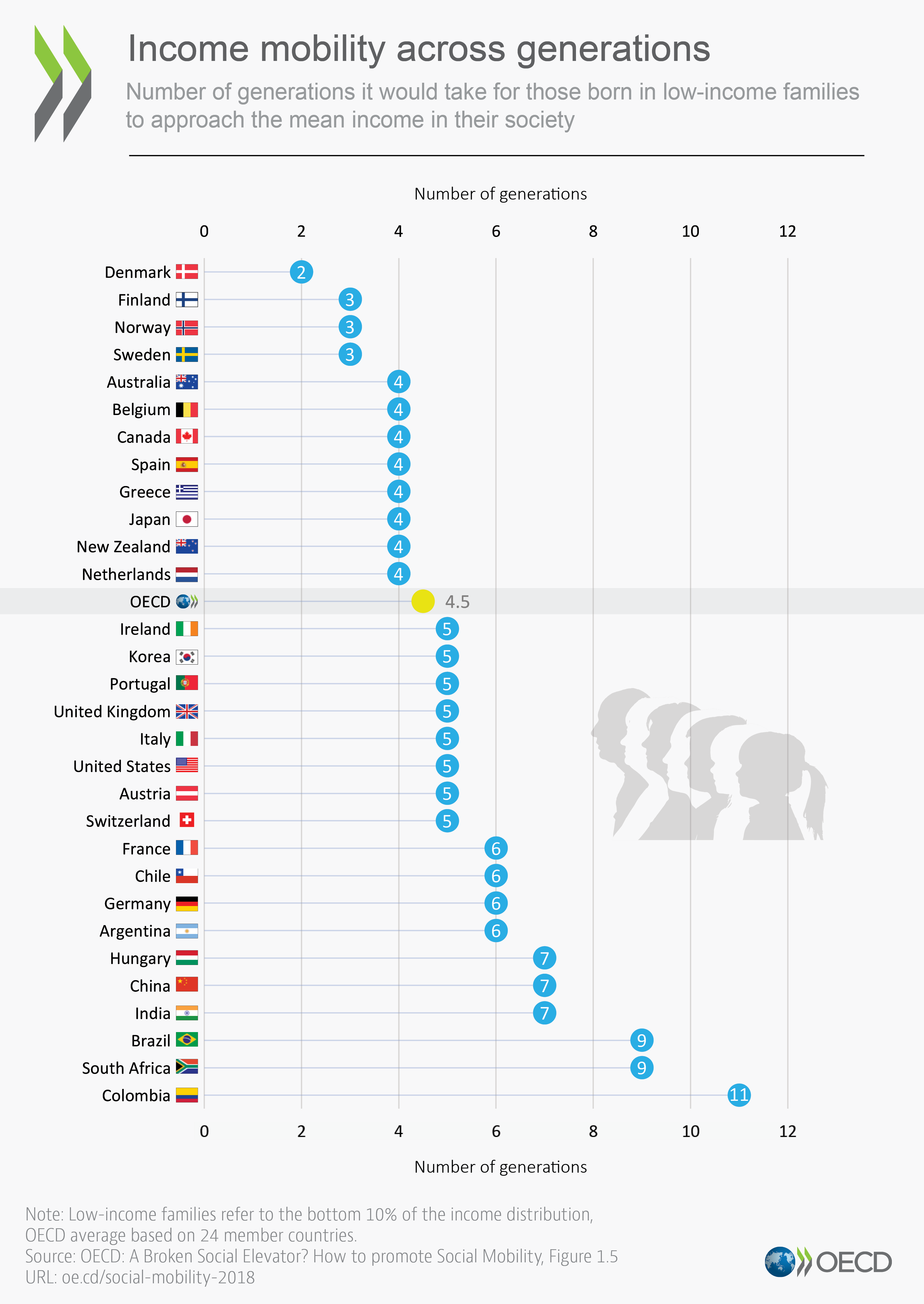

There are plenty of problems with this. It’s not just that the right has been pushing the social mobility argument “since the dawn of time,” in economist Dean Baker’s words, which makes it more of a lukewarm take. Baker summarizes this argument as, “don’t worry that your standard of living is awful, the important thing is that your kids will be able to get rich.”

Except that they probably won’t. As Lowenstein acknowledges, social mobility has declined in this country. What he fails to mention is that, despite our self-mythology as “the land of opportunity,” social mobility in the United States lags behind most of the Nordic countries and several Western European nations. And it’s been getting worse for some time.

That’s where Blankfein comes in, according to Lowenstein. Blankfein’s story “should be an inspiration,” writes Lowenstein, because his father was a postal worker and he “made it to Harvard and then to the top of Wall Street.”

Pretty boy Lloyd

Lowenstein neglects to mention how Blankfein “made it to the top.” Under his leadership, Goldman Sachs engaged in a pattern of systematic fraud that led to billions of dollars in settlements and fines.

An “inspiration”? Under Blankfein’s leadership as CEO, and before that as COO, Goldman Sachs committed the deeds that led to:

A settlement of more than $5 billion for systematically defrauding investors in its mortgage-backed securities. (Yes, the settlement was a “sham,” but it offers a glimpse into the magnitude of Goldman’s crimes);

A $650 million fine for the ABACUS fraud, where it sold mortgage-backed securities to investors without telling them that they were hand-picked by someone who was betting against them;

A $330 million settlement for abusive foreclosures;

A $120 million settlement for manipulating the foreign exchange market;

An arbitration assessment of more than $20 million for helping to facilitate a Ponzi scheme;

And, a fine of $650,000 for failing to disclose that two of its traders were under investigation by the SEC.

This is only a partial list (more here), but it should be more than enough to convince most reasonable people that Blankfein is not someone to emulate.

Then there’s the small matter of perjury. A Senate panel concluded that Goldman Sachs committed criminal offenses, and recommended that perjury charges be brought against Blankfein. Blankfein hired a defense attorney, but the Obama Administration’s reluctance to prosecute senior Wall Street executives apparently spared him the discomfort of a trial.

Some inspiration.

But at least Goldman Sachs pays its taxes, right? Not so much. A 2016 report by Citizens for Tax Justice found that “Goldman Sachs reports having 987 subsidiaries in offshore tax havens, 537 of which are in the Cayman Islands despite not operating a single legitimate office in that country, according to its own website. The group officially holds $28.6 billion offshore.”

Yes, it’s inequality

Despite this rather dubious record, Rosenstein argues that “policies designed to increase the number of Blankfeins will do more good than policies designed to level income disparities.”

To be fair, Rosenstein isn’t arguing for the proliferation of fraud or alleged perjury or proposing to clone the retiring CEO. Rather, he’s arguing in favor of Blankfein’s wealth – because, he argues, “more people working at good salaries cannot be a bad thing.”

Except that it can, if those people are driving the cost of living beyond the reach of millions of Americans. A number of economists have confirmed that inequality is harmful (see here, here, and here, for starters) and that the causes include “globalization and the decline of labor unions” (two factors Rosenstein dismisses), but Rosenstein doesn’t mention them.

As a countervailing authority, he cites only Gallup in-house economist Jonathan Rockwell. That is not persuasive, to say the least.

Yes, it’s Wall Street

Rosenstein also writes this: “It’s also far from proved — to me, it’s not even intuitive — that high incomes on Wall Street and elsewhere are the reason for, say, flatter wages in manufacturing.”

It happens in several ways. First, Wall Street’s higher incomes are largely driven by short-term investment strategies. These strategies often emphasize layoffs and other cost-cutting measures over long-term investment in areas like manufacturing. Secondly, hedge-fund investors are as likely to bet against job-creating industries as they are to bet for it – and will then do whatever they can to protect their bets.

Then there’s the matter of the financial crisis, which was primarily the product of Wall Street firms like Blankfein’s. The recovery from that crisis has been lopsided, with only upper-income households seeing an increase in their median wealth. Middle- and lower-income families are worse off, and the wealth gap between upper-income families and everyone else is now the ever recorded.

Lowenstein’s essay does what many conservative arguments do: it argues for an artificial division between the questions of income inequality and social mobility. There is ample research to suggest that the two problems are inextricably conjoined. Higher inequality leads to lower social mobility. If you’re concerned with one, you should be equally concerned with the other.

Bankers of a lesser God

Who knows? Maybe Lowenstein is just trolling Blankfein’s many detractors. Whatever his motives, his argument doesn’t hold up.

Blankfein certainly doesn’t need the help, although he does say he’s “on the job market.” He escaped prosecution, after all, and he’s retiring to a reported $85 million payout. There’s no sign that Blankfein intends to enter government, even though many other Goldman alums have joined (or cycled through) the Trump administration. He was a Hillary Clinton supporter, but said in February that the economy is “probably higher” than it would have been had she been elected.

“I haven’t felt this good since 2006,” Blankfein said.

Lowenstein seems to be making the same case Blankfein made in 2009, when he famously said he was doing “God’s work” by engendering a “virtuous cycle” of “growth and more wealth.”

But it’s not true. Blankfein and his peers are strangling genuine growth, turning a productive economy into a financialized one, and driving up already-unsustainable levels of inequality. Blankfein is retiring to a rather sizeable earthly reward, but he shouldn’t expect gratitude from any fair-minded deity.

Get NationofChange in your inbox

Independent reporting every weekday. No paywall, no advertisers, no corporate owner. Free, and you can unsubscribe whenever you like.

Subscribe freeYour gift is being matched, up to $2,000.

A member of the NationofChange board is matching every contribution to our summer drive, dollar for dollar, until the $2,000 is used up or the drive ends on 24 August. We take no advertising money and answer to no corporate owner. The article you just read was paid for by readers, and right now what they give counts twice.

{kind=link}

{kind=link}

COMMENTS