SIDNEY, Ohio – Toward the end of last summer, managers at global giant Emerson Electric Co. called an employee meeting at its air conditioning and refrigeration factory in this county seat of 21,000 people west of Dayton. They had big news: Each employee would get a $1,000 “special contribution” to a 401(k) retirement account.

The reason for the generosity? The Tax Cuts and Jobs Act congressional Republicans had passed, and President Donald Trump had signed in late 2017, Emerson executives told the Sidney plant employees.

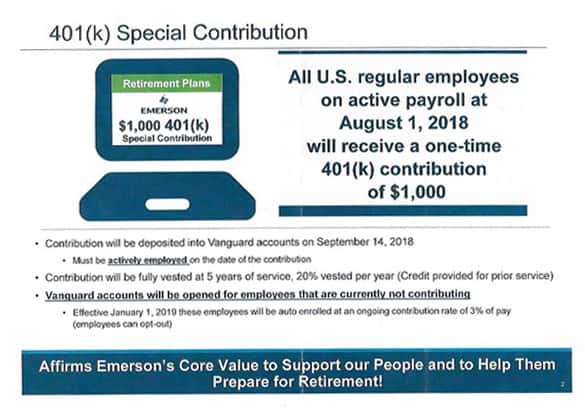

With the announcement, Emerson joined hundreds of companies – as many as 750 by one count – that issued similar statements to show they were sharing the wealth of a $150 billion cash windfall firms were estimated to receive in the first year from the then newly-enacted tax law. On an employee bulletin board, Emerson explained in bold type that the contribution “Affirms Emerson’s Core Value to Support our People and to Help Them Prepare for Retirement!”

That’s what has made the promise of higher compensation so far elusive. The Bureau of Labor Statistics reported nominal wages increased 3.2 percent in January year over year, and by less than one percent – three cents to $27.56 – month over month. While some economists have voiced enthusiasm about the improvement, other economists note that wages must grow for a sustained period to offset decades of stagnation. One year is “not sufficient,” said Seth Harris, deputy secretary of the Labor Department in the Obama administration. “The problem has not been solved.”

Bonuses have registered less of an impact, increasing just 2 cents an hour in the first nine months of 2018, according to Lawrence Mishel, former president of the Economic Policy Institute, a left-leaning research group.

The increase was “imperceptible,” Mishel wrote in December on EPI’s blog. “Whatever growth in bonuses has taken place is not necessarily attributable to the tax cuts, rather than employer efforts to recruit workers in a continued low unemployment environment.”

“Whatever growth in bonuses has taken place is not necessarily attributable to the tax cuts, rather than employer efforts to recruit workers in a continued low unemployment environment.”

Lawrence Mishel, former president of the Economic Policy Institute

By all accounts, companies poured a hefty portion of the tax windfall into buying back shares, a move designed to at least temporarily boost stock prices, which benefits executives and other large stockholders. And buybacks, evidently unlike bonuses or wage increases, will certainly continue; Goldman Sachs estimates corporations spent a record $770 billion in 2018 on repurchasing stock and will increase that to $940 billion this year. Other chunks of the cuts went to dividends or reducing debt.

A promise of ‘more money’

Back at Emerson, as managers unveiled the news at the Sidney plant that makes Copeland Scroll branded products, longtime employee Lerouise Rupert, 32, said she was excited at first. “I’m thinking, ‘This is going to be good.’ They told us, ‘We’re going to give you a $1,000 bonus,’” Rupert said recently while sitting with her three children in a nearby Wendy’s Restaurant.

Then Emerson managers explained the details. The bonus wasn’t being awarded in cash because “‘it would get taxed a lot,” recalled Rupert, whose job runs from driving a forklift and loading the assembly line to building electrical boxes. So instead, they said, “We’re going to put it in a 401(k) for you.’”

The contribution has had little tangible benefit for Rupert, who has a company pension but did not have a 401(k) account at the time, and for many of her co-workers. Their real need is for money immediately to pay bills, or in Rupert’s case at the time, the chance to buy presents for her children instead of signing up for a local charity gift program.

Rupert’s experience provides a stark contrast to how Trump and Republican lawmakers sold the tax law. “You’re going to start seeing a lot more money in your paycheck,” Trump said a year ago at an event in Nashville, Tennessee. A couple months earlier, Trump, and then-House Speaker Paul Ryan, R-Wis., boasted the tax law would likely give typical households a $4,000 a year wage hike, with the White House reporting wages could even increase by more than $9,000 a year.

Manufacturing executives were particularly vocal, arguing that the lower corporate tax rate would not only increase wages, but also allow their companies to be more competitive globally and bring back jobs. David Farr, chief executive of Emerson Electric and former chairman of the powerful National Association of Manufacturers, helped lead the tax-cut effort and pushed for a lower 15 percent corporate tax rate.

Emerson, based in Ferguson, Missouri, employs approximately 87,500 people worldwide, with about 24,000 employees in North America.

Last May, five months into the new law, Farr told Congress, “Tax reform is helping strengthen communities, build new career opportunities and increase paychecks for the men and women of America’s manufacturing workforce.”

An Emerson spokeswoman said Farr was not available for an interview.

Emerson’s tax rate fell to 17 percent in 2018, under the new tax law, according to its year-end filing with the Securities and Exchange Commission; Emerson executives estimate a tax rate of 24 to 25 percent this year, boosting profits year over year. Farr told investors in an August presentation on quarterly earnings that the tax law allowed the company to increase wages and improve the company’s health plan, parental leave and paid time off.

But Emerson reported it received $189 million in tax savings, of which it spent $24 million, less than 13 percent on its 401(k) bonus contributions – a payment that brought financial benefits to the company as well. Emerson also spent $1 billion – more than 40 times the amount it spent on the retirement bonuses – in its fiscal 2018 buying back its own shares.

And for those on the ground, Emerson’s largesse appears limited.

That’s what employees say at Ridge Tools, an Emerson subsidiary in Elyria, outside Cleveland. The company has a commanding presence in the struggling town of 54,000, with its own water tower emblazoned with the word “Ridgid,” the brand name of the power tools the company makes.

Several Ridge Tool employees, who asked to remain anonymous, told the Center the corporate tax cuts have not increased their salaries. They have received the same annual increase in their wages as in past years: less than 3 percent. Emerson recently increased the vacation time to three weeks from two weeks for employees who have been employed for at least five years, they said. Hourly employees at the Sidney plant receive an annual 3 percent increase under the union contract. An Emerson spokeswoman said the company is spending $3 million annually on improved benefits but declined to provide details. The spokeswoman said the company provides “market-based pay increases.”

Ridge Tool workers also received that $1,000 retirement contribution, and not all were disappointed. Joe Neudenbach, a longtime employee, said he had planned to withdraw the money – at 61 years old he can without paying a penalty – to buy a new recliner to watch the Super Bowl played earlier this month. “The $1,000 was cool. I didn’t see it coming,” said Neudenbach, who added that he gets about $30 a week more in his paycheck because of the lower rates for individuals in the new tax law.

Still, the one-time bonuses and one-time 401(k) contributions have been widely panned as public relations stunts that are not financially sustaining like annual wage increases. Longtime pensions and retirement expert J. Mark Iwry said employers cut or suspended 401(k) contributions in the 2008-2009 recession, but it appears most have now been restored.

“By the same token, following last year’s major corporate tax cut, with the promise of employer tax benefits flowing through to workers,” Iwry said, “it would seem appropriate for employers to share their tax savings with their workers – for example, through new employer 401(k) plan contributions or wage increases.”

Bonuses, then layoffs

Some claim the Tax Cuts and Jobs Act was indeed a windfall for employees in 2018. The conservative Americans for Tax Reform group kept a running tally of corporate announcements through last October and listed as many as 750 examples of “pay raises, charitable donations, special bonuses, 401(k) match hikes, business expansions, benefit increases, and utility rate reductions attributed to the Tax Cuts and Jobs Act.”

But shareholders have fared far better than employees under the tax law. Companies spent $929 billion on stock buybacks compared to $7.1 billion on wage increases and bonuses, according to Americans for Tax Fairness, a left-leaning nonprofit group that tracked announcements by Fortune 1000 companies.

Another report by the nonprofit Just Capital, which tracks the Russell 1000 Index, which includes the largest U.S. public companies, found that 145 companies in the index announced plans for spending the cash windfall, and only 6 percent of spending was allocated to workers, “more than half of which takes the form of one-time bonuses, as opposed to permanent raises or benefits.”

Companies also used the tax savings to pay down debt. The percentage of cash outflows that businesses applied to debt increased from 5 percent before the tax bill to 37 percent after the law went into effect, according to Moody’s Investors Services.

Among the first companies to come out with announcements of bonuses and pay raises because of the tax law were Walmart and AT&T. On Jan. 11, 2018, Walmart announced it was giving out $1,000 one-time bonuses to eligible employees and increasing its starting hourly wage to $11, a move that many attributed more to competition than the tax law. The same day, Walmart filed notices to lay off thousands of workers. A Walmart spokesman said the company has no current plans for a 2019 company-wide bonus. He said the hourly employees’ average total compensation and benefits is more than $17.50 an hour.

On Dec. 20, 2017, two days before Trump signed the tax law, AT&T CEO Randall Stephenson announced the tax law would allow the company to give one-time bonuses of $1,000 to each of its workers at a cost of $200 million – about 1 percent of the estimated $20.4 billion tax windfall the company recorded in the fourth quarter of 2017. While handing out the bonuses, AT&T was in the middle of laying off thousands of workers, including employees at call centers in Indiana, Texas and Michigan.

“Employees who have been there and built the company are being pushed out in the chase of the almighty dollar,” said Marvin Thompson, who has worked for AT&T for 18 years in its Dayton, Ohio, center.

An AT&T spokeswoman said the company would not be handing out another bonus this year, but the company made, in addition to the bonuses last year, an $800 million investment in its employee and retirement medical trust, and $100 million to its foundation.

By this time last year, a number of companies from The Walt Disney Co. to Lowe’s and Southwest Airlines had announced they would use a portion of the tax windfall to give one-time employee bonuses. Southwest said it would use $55 million of its $1.3 billion tax windfall on bonuses. At the same time, it spent $2 billion on buybacks in 2018. Disney received a $1.7 billion benefit and paid out $125 million on employee bonuses – and $3.6 billion on share repurchases. None of the companies have announced another round of bonuses. Southwest said it had no plans to give bonuses this year and Lowe’s did not respond to requests for comment. Disney referred the Center to its January 2018 announcement.

Will it work – later?

To have the tax cuts translate into increased wages, the theory goes, several factors need to align. Republicans and corporations argued the tax cuts would lead to increased investment in factories and machinery. That would create more productive and valuable workers, which “would bid up the wages,” said Mark Mazur, head of the nonpartisan Tax Policy Center in Washington. But for that to happen, “every linkage has to work,” he said.

Meanwhile, in Sidney, Rupert is still trying to cash out her $1,000 retirement contribution, which was the only deposit in her 401(k) account because she didn’t have one when Emerson gave out the bonuses last year.

Rupert said she is willing to pay the penalty for an early withdrawal but she hasn’t gotten far with her inquiries.

A frustrated Rupert said the last time she checked her account the balance was just $867, a likely victim of the stock market fluctuation.

{kind=link}

{kind=link}

COMMENTS