There’s a lot that you should know about the Republican Medicare plan, a plan that Speaker Paul Ryan (R-WI) hopes to enact shortly after President-elect Donald Trump takes office, but the entirety of it can be summarized in just one sentence.

Republicans want to charge seniors a lot more for inferior health coverage.

Over the last half-decade, Ryan has proposed several different versions of the Republican plan to charge seniors a lot more for inferior health care. There are important differences among these versions. Some would phase out Medicare entirely over the course of many years, while others would merely make the system more inefficient and drive out-of-pocket costs for seniors much higher. The most recent version is impossible to fully evaluate because it lacks important details — like numbers.

As Jonathan Cohn and Jeffrey Young quipped about the GOP’s overall health care package, “Speaker Paul Ryan wants to replace 20 million people’s health insurance with 37 pages of talking points.”

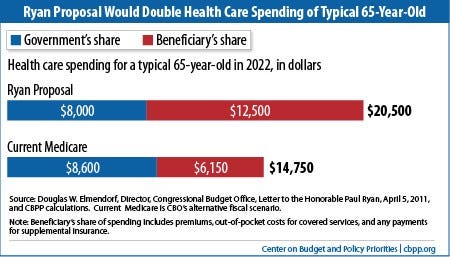

Despite the differences, however, all of Ryan’s proposals would impose basically the same structure. Republicans hope to repeal Medicare — the single-payer system that most seniors rely on to cover their health costs — and replace it with a voucher. This voucher will cover some of the cost of inferior coverage that will leave seniors with higher out-of-pocket costs than they would have paid under traditional Medicare. As a bonus, the total cost of paying for an individual senior’s care — that is, the government’s share of the costs plus the individual’s share — could rise as much as 40 percent.

Inferior coverage at a higher price — that’s the Republican health plan. And it will become law unless three of the 52 Republican senators who will come to Washington in January decide to stop it.

Why Ryancare can’t work

Paul Ryan, the architect of the Republican Medicare plan, brings a fundamentalist’s zeal to his free-market faith. And he does not temper this deal with basic arithmetic.

Indeed, Ryan once offered a plan to privatize Social Security that, if implemented, would have required the federal government to purchase so many private investments that “by 2050, every single stock or bond in the United States would be owned by a Social Security account.”

That’s right. In his eagerness to turn over as much of our government as possible to capitalist markets, Ryan unintentionally offered a plan to transform the United States into a socialist nation. Nice work, Comrade.

So Paul Ryan is not a numbers guy. He is long on theory, long on confidence that the market shall provide a solution, and short on knowledge of the subtle details of policy making that, for example, prevent a proposal to invest some of seniors retirement funds in private investments from becoming an accidental plan to have the government seize the means of production. Perhaps that explains why Ryan’s Medicare plan would charge seniors a lot more for inferior health coverage.

Again, it’s impossible to know exactly how much more seniors will pay for inferior health coverage under the Republican Medicare plan, because Paul Ryan hasn’t exactly been forthcoming with figures like how much the vouchers will be worth or how much he expects his proposal to cost. In 2011, however, Ryan did provide enough information to allow researchers at the Center on Budget and Policy Priorities to calculate how much costs would increase for seniors. Their conclusion was grim.

There are two reasons why moving more seniors into private health plans will jack up the overall cost of care. One is that private insurers simply have far more administrative costs than a government plan. The other is that traditional Medicare has far more power to bargain down health costs than private insurers.

One of the most important mechanisms for keeping down health care costs is a bargaining process that takes place between insurers and health providers.

When a large health insurer is confronted with a six figure bill for a lung transplant, or even a three figure bill for a patient’s anti-fungal drugs, they are typically able to bargain these prices down because they speak on behalf of thousands, tens of thousands, or even hundreds of thousands of patients. If a particular hospital refuses to bargain, an insurance company can threaten to cut that hospital out of their network, so the hospital will come to the negotiating table out of fear that it will lose a large chunk of its patients.

An insurer’s power in this negotiation, however, is directly related to the number of patients it represents. A hospital may be able to afford to lose business from a small insurer, and thus is more likely to drive a harder bargain with such an insurer than it would with a larger insurer that can speaks on behalf of many more patients. And the biggest insurer of them all, at least in the United States, is Medicare.

In 2010, seniors accounted 34 percent of health care costs in the United States, despite making up only 13 percent of the population. Mortality being what it is, people will unavoidably spend more on medical care as they age, so a health plan that covers the bulk of America’s seniors will command significant bargaining power against hospitals. Few health providers can afford to simply give up payments from Medicare patients, so they need to agree to the prices that Medicare is willing to pay.

What Paul Ryan wants to do is divide up the powerful bargaining unit of seniors currently covered by traditional Medicare into dozens of smaller private health plans. That leaves each of these health plans with far less power to drive a hard bargain. The result is more money for hospitals and higher out-of-pocket costs for seniors.

Republicans, in other words, want to charge seniors a lot more for inferior health coverage.

Phasing out Medicare

An open question is whether Ryan intends to simply charge seniors more for inferior coverage, or if he will actually phase out Medicare itself — leaving seniors with an increasingly worthless voucher in lieu of the robust health coverage they currently enjoy.

During the debate over Obamacare, the phrase “bending the cost curve” was frequently tossed around. This refers to the biggest long-term problem facing health policy makers: for most of the last four decades, health care costs have grown faster than wages. Indeed, the numbers here are quite stark. Between 1960 and 2012, health costs grew from 5.2 percent of GDP to 17.9 percent. One of the primary reasons why so many Americans haven’t felt any real wage growth for decades is that their raises are being eaten up by higher insurance premiums and doctors’ bills.

Bending the cost curve meant reducing the rate of health inflation so that it no longer consumed a larger share of Americans out-of-pocket costs every year. And there are early signs that this cost curve did begin to bend downward under President Obama.

Ryancare, by contrast, risks shifting this curve upward for the reasons explained above — it diminishes Medicare’s ability to bargain prices down.

Ryan has taken conflicting positions on whether his new voucher program will account for the cost curve. In 2011, Ryan’s original health plan provided that the new Medicare vouchers would gain value each year at a rate that was slower than the rate of health inflation — effectively causing them to lose value with each passing year. According to the Congressional Budget Office, “by 2080, Medicare would be cut 76 percent below its projected size under current policies” if Ryan’s 2011 plan had become law. A child born in 2015 would receive less than a quarter of the resources provided to today’s seniors when that child became eligible for a voucher.

By contrast, the most recent version of Ryan’s Medicare plan provides that the value of the voucher should be determined “based on the average bid of participating plans.” So the voucher would be indexed to something that is likely to rise at close to the rate of health inflation. The latest version of Ryancare would charge seniors a lot more for inferior health coverage, but it doesn’t appear to phase out Medicare in the same way that the 2011 version did.

Nevertheless, given the increasing vagueness of Ryan’s plans, the speaker’s oft-demonstrated innumeracy, and the fact that he can’t seem to settle on the details for how he plans to voucherize Medicare, it remains an open question whether the vouchers would lose value over time.

The three most important people in America

So, to summarize, Republicans plan to charge seniors a lot more for inferior health coverage. They will do so in a way that will jack up the total cost of care in the United States. And they could potentially cause America’s historic commitment to seniors’ health care to slowly vanish over the course of many years.

The architect of this plan is a man so drunk on conservative ideology that he often does not even bother to check the math underlying his proposals — or even to include numbers in his proposals so others can do so. And Republicans will soon control both houses of Congress and the presidency.

The future of Medicare looks grim.

There is, however, a potential way out. When the new Senate is seated this January, Republicans will control only 52 seats in the likely event that they win a runoff in a still-undecided race of a Louisiana senate seat (if the Democrat prevails in this race, Republicans will only control 51 seats). That means that just three Republican senators can save America’s seniors from Paul Ryan.

It will be a heavy lift to convince three Republicans to do so. The Senate has only grown more polarized since President George W. Bush’s plan to privatize Social Security was defeated in 2005. And Republican moderates haven’t exactly been the picture of courage since Donald Trump was chosen as the party’s nominee.

Nevertheless, every Republican senator has a choice to make. They can be one of the people who destroyed Medicare, or they can be one of the people who saved it. And it only takes three of them to keep Medicare in place.

Get NationofChange in your inbox

Independent reporting every weekday. No paywall, no advertisers, no corporate owner. Free, and you can unsubscribe whenever you like.

Subscribe freeYour gift is being matched, up to $2,000.

A member of the NationofChange board is matching every contribution to our summer drive, dollar for dollar, until the $2,000 is used up or the drive ends on 24 August. We take no advertising money and answer to no corporate owner. The article you just read was paid for by readers, and right now what they give counts twice.

{kind=link}

COMMENTS